Walls & Ceilings State of the Industry

Walls & Ceilings magazine loves attending trade shows to see what new products are being introduced. As we’ve seen the attention towards products by R&D still focusing on labor, power tools have become more ergonomic, materials such as drywall has become lighter, steel framing assemblies offer faster ease of installation, lasers are self-calibrating and offer more bells and whistles, etc. But it’s talking to the manufacturers and contractors that offer us the best pulse on the modern contractor of the 21st century. While walking the show floors to talk with people, it seems that everyone wants to know how everyone else is doing.

In 2014, the industry made a larger climb in growth than in the past five years. Profit margins are up, contractors are bidding (and securing more jobs), distributors are selling more product.

Walls & Ceilingsconducted its own in-house State of the Industry survey to hundreds of contractors in five regions across the country. These contractors were asked about everything from challenges (labor, employee benefits, bidding) to the residential vs. commercial market, technology and much more.

As our State of the Industry survey makes clear, there are a number of important challenges still facing the wall and ceiling community. We asked industry experts to single out what they feel are the most critical obstacles in the year ahead and share their advice on overcoming them. Most commentators focused on the economy, the labor market, increased competition and governmental regulations as key areas of concern.

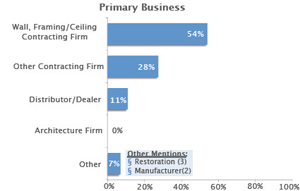

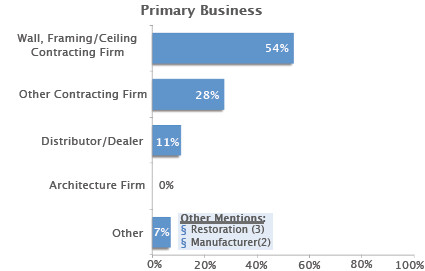

For this survey, the primary business contacts were divided up into these four groups:

- Wall and ceiling contractors: 54 percent

- Other contracting firms (GC, various other contractors): 28 percent

- Dealers/distributors: 11 percent

- Other groups (restoration/renovation contractors, manufacturers): 7 percent

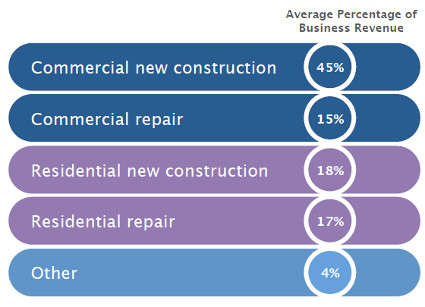

Of these groups, 45 percent were commercial contractors; 15 percent commercial repair; 18 percent accounted for residential; 17 percent was residential repair and 4 percent accounted for various other areas.

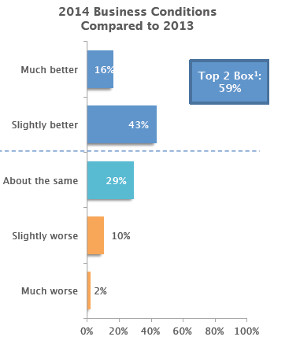

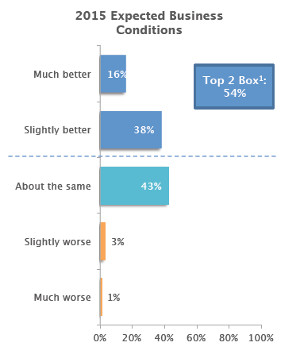

More than half of the respondents indicated business conditions were better in 2014 than last year, and 54 percent expect business conditions to be slightly better or the same next year.

- Much better: 16 percent

- Slightly better: 38 percent

- About the same: 43 percent

- Slightly worse: 3 percent

- Much worse: 1 percent

Eighty-six percent of the respondents indicated the cost of doing business has increased this year compared to 2013, and 86 percent expect the cost of doing business to increase next year.

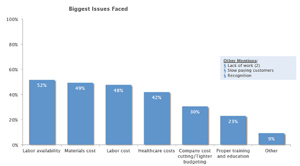

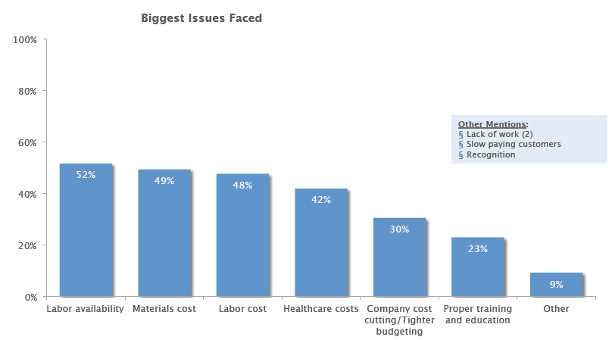

Out of the hardest challenges that face our industry, half of the respondents indicate their company is facing labor availability issues and /or material cost issues:

- Labor availability: 52 percent

- Materials cost: 49 percent

- Labor cost: 48 percent

- Healthcare costs: 42 percent

- Company cost cutting/budget cuts: 30 percent

- Training and education: 23 percent

- Other (lack of work/tardy payments/overhead): 9 percent

For contractors’ annual gross sales, the majority of companies’ 2014 sales were expected to increase overall compared to 2013, with an average expected increase of 22 percent.

Economic conditions are expected to be the most influential factor in 2015, followed by lowball pricing/bidding wars and costs of healthcare:

- Economic conditions: 76 percent

- Lowball pricing/bidding wars:

- 62 percent

- Costs of healthcare: 61 percent

- Finding qualified workers: 53 percent

- Material costs: 52 percent

- Cash flow/financing: 48 percent

- Government intervention/regulation: 48 percent

- Costs of insurance (not including healthcare): 44 percent

As the wall and ceiling industry recovers from an arduous and bleak market, the overall summary is there is an improvement amongst contractors. Many companies report projects from six to more months out. Jobs booked more than half a year out suggest a better market than conditions that some contractors faced just two years ago, such as competitors low bidding and hand-to-mouth work schedules that were always uncertain from month to month.

|

|

The majority of respondents work for wall, framing/ceiling contracting firms. |

As you’ll read in the sidebars from industry manufacturers, demand is on the rise and profit margins have steadily risen for the past year to two years.

The industry may never see the levels of the mid-2000s to 2008 again; but those were exceptional times. All indicators from this survey to other independent studies suggest that the construction market overall (which certainly includes wall and ceiling contractors) should breathe easier as the next few years suggest a healthy climate.

Tom Porter Executive Vice President, CEMCO

|

|

The majority of commercial business revenue comes from new construction, while residential business revenue is split relatively evenly between new construction and repair. n=174 Means reported above; Q110. What percentage of your business revenue comes from the following? |

W&C: How is business now compared to 2013? Better or worse?

As business volume appears to be rising, margins are running in the opposite direction for all product groups.

W&C: Is the residential or commercial market stronger for you as of this year?

Despite the increase in residential starts this past summer, we haven’t seen any measurable increase in volume from the major builders in the majority of our markets. Given that, we have seen an up-tick in the commercial sector, but as stated before, margins continue to compress as volumes move up ever so slightly.

W&C: How has the current construction climate been in your region and for you as a company?

We are seeing a significant increase in builder confidence, which translates into an increase in opportunities to quote new projects for the upcoming 2015 year and beyond.

W&C: What are your forecasts for next year? Up, down, flat?

Our research is indicating an increase in volume in most of our markets. Some markets may be more robust than others but an overall increase of about 5 percent is what we anticipate. However, the continued pressure of higher costs from domestic steel mills is going to challenge profitability for the near term.

W&C: How are you reaching your customers? Social media? Face to face? Distributors/dealers?

Our most effective vector to our customers still remains face-to-face. Social media, even with its increasing popularity, still has yet to produce substantial gains in terms of new customers, increased communication, and more effective penetration into new geographic areas for us.

Joann Davis Brayman Vice President of Global Marketing, Armstrong World Industries

W&C:Is business better than it was in 2013?

In North America, we were like many building material companies that saw business impacted by the weather early in the year. This included jobs that were delayed and shipments of products that were negatively impacted. But generally throughout the year we have seen some slight strengthening relative to 2013.

W&C:Is the residential or commercial market stronger for you as of this year?

We are more driven by the commercial markets, and while there has been a slight improvement in the new residential segment, our residential business is more tied to residential remodeling.

W&C:How has the current construction climate been in your region and for you as a company?

Our presence is global with a strong business base in both U.S. and Canada. We definitely see a lumpy recovery across the different regions of the U.S. and Canada and within the different commercial and institutional building segments (office, education, healthcare, etc.)

|

|

More than half of respondents indicate business conditions are better in 2014 than in 2013, and 54% expect business conditions to be slightly better or the same in 2015. n=174 1Top 2 Box (Slightly/Much better) Q115. Overall, how have wall and ceiling industry business conditions been the first 6 months of 2014 compared to the first 6 months of 2013? |

W&C:What are your forecasts for next year? Up, down, flat?

Many of the key macros indicators that we look at such as the Architectural Billing Index, the McGraw Hill Momentum Index, government data such as Construction-Put-In-Place, have been positive recently, which is a good sign. But we have not yet worked through the fine points of our planning process to have a formal view on the opportunity in 2015.

W&C:How are you reaching your customers? Social media? Face to face? Distributors/dealers?

We use all of these methods to reach our customers. Digital media is an expanding opportunity to target our customers but we also use more traditional methods of face-to-face and print. We work hard to deliver our messages in the ways that our customers want to receive them, providing them choices.

Dennis Deppner Technical Services Manager, Master Wall Inc.

Compared to 2013, Deppner reports business for Master Wall has seen a substantial improvement compared to 2013 with steady orders even during historically slow times. The company reports steady to robust activity with their applicators.

W&C: Is the residential or commercial market stronger for you as of this year?

Commercial projects are leading the way this year along with increases in multi-family residential and an uptick in large residential building.

|

|

More than half of respondents indicate business conditions are better in 2014 than in 2013, and 54% expect business conditions to be slightly better or the same in 2015. n=174 1Top 2 Box (Slightly/Much better) Q120. Overall, how do you expect business conditions to be in the first 6 months of 2015 compared to the first 6 months of 2014? |

W&C: How has the current construction climate been in your region?

We sell internationally. The southeast to Texas has been the strongest region in the U.S. and sales to China have been strong.

I'd describe the mood as cautiously optimistic but based on 2014 that’s an understatement. We've added new distribution and are growing in new areas. Sales will be up.

W&C: How are you reaching your customers? Social media? Face to face? Distributors/dealers?

Distributors are our primary contact with our customers. We support them and our applicators through our sales force and technical support. We’re also active on Facebook and LinkedIn.

|

|

Half of respondents indicate their company is facing labor availability issues and/or material cost issues. |

Fred Daniels III CEO, Ames Taping Tools

Two years into his role as CEO of AMES Taping Tools, Fred J. Daniels III is still enthusiastic about the construction industry, as housing starts and commercial building projects continue to gain momentum.

The economy has breathed new life into multi-family housing and the commercial sector, and there are pockets of growth in residential construction that should help lift the number of jobs for finishing contractors, says Daniels, who assumed the helm in October 2012, following one of the steepest declines in history for construction activity.

Part of Daniels’ vision for the company is expanding its retail network, both by returning to previous market positions and identifying new growth areas. To this end, Daniels says that the company hopes to open 14 new storefront locations by the end of 2015, mostly around the Eastern and Southern corridors.

Aside from expansion, Daniels plans to continue to grow the “one-stop-shopping” convenience that has been a company hallmark since Bob and Stan Ames began visiting job sites to tout the time-savings and efficiency advantages offered through automatic taping technology.

|

|

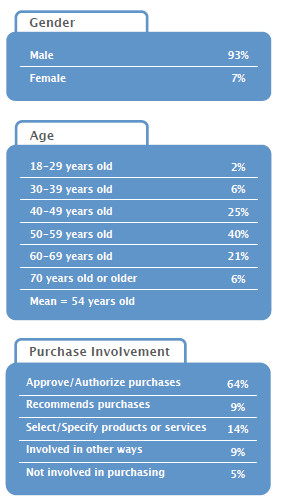

Respondent Profile n=174 Q905. In what year were you born? Q910. Please indicate your gender. Q935. Which of the following best describes your usual involvement in your company’s purchases? |

In addition to the productivity gains offered by automatic taping and finishing tools, an often overlooked means of greater efficiencies—and profits—are the tools themselves.

“Based on our data, culled from conversations with hundreds of contractors nationwide, job-ready tools can boost productivity by up to 15 percent,” reports Daniels. “Using an average hourly labor rate of $47, this added performance can translate into $282 extra per worker, per week. For a crew of three, top-quality tools can help generate an additional $44,000 in billings annually.”

“The economy has really forced a reset for our industry,” explains Daniels. “Many contractors and trades people who led the industry during the housing boom of 2005-2007 have left and moved into other vocations. As a result, drywall contractors are now faced with a pressing need to train new finishers and make them more productive with efficient tools and finishing practices.”

Daniels is dedicated to collaborating with local trade unions to create certification programs to train professionals in the use of tools. The company also continues to offer free training every other month at its Stone Mountain, Ga., headquarters, as well as on-the-job-site training across the country.

Kurt Riesenberg Executive Director, Spray Polyurethane Foam Alliance

Unique in the sense that the SPFA is reporting as an association of its members, Riesenberg says improvements have been made over last year.

“Based on SPF material sales data across the U.S., business is up approximately 15 percent year over year,” he says. “While the industry continues to see growth opportunities in the higher-end new residential and commercial construction markets, this remains a challenging time for SPF businesses, as well as all construction-related businesses. However, our SPF contractor members commonly state that they have more work pre-planned for early next year than in recent years, which the industry looks to as a sign of anticipated strong performance for 2015 and beyond.”? ?

|

|

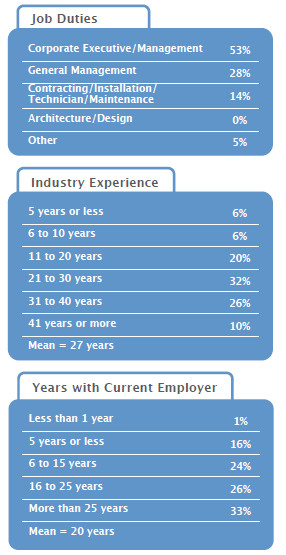

Respondent Profile Q915. Which of the following most closely describes your job title? Q916. Approximately, how many years of experience do you have working in the wall and ceiling industry? Q940. How many years have you been with your current employer? |

When asked whether the residential or commercial is stronger, Riesenberg says it’s difficult to tell, because the industry only tracks product sales, not installation by building type. “That said, SPF is a draw to both markets for different reasons,” he says. “In the case of residential, the higher-end new construction sector maintains strong demand for spray polyurethane foam insulation, supplemented by energy-saving renovations to existing home attics and crawlspaces, locations where buildings typically realize over 40 percent of their energy losses. Additionally there are various government-issued energy efficiency investment incentives for residential construction and renovation that help to lower the first-cost of SPF.

“In the commercial sector, overall construction demand has typically been down but recent falling vacancy rates mean that businesses will require more office space in coming years,” Riesenberg says. “Specifically, both spray polyurethane foam insulation and roofing enjoy overall strong demand due to the energy savings, and structural and architectural benefits of the product. Owners looking for a high-performance solution with favorable bottom line financials, tax deductions and incentives, migrate toward the SPF product.”

The association estimates sustained growth in 2015.

Greg Salah Senior Vice President of Sales and National Accounts, USG

Chicago’s U.S. Gypsum also reports that business conditions improved for manufacturers in 2014. He says that wallboard demand has increased about 5 percent and it appears the company is in the early stages of a steady recovery in the construction sector.

Salah says that residential housing starts are up, leading to a better market. Meanwhile, the commercial market has modestly improved from earlier in the year when one of the nation’s worst-ever winters in many parts of the country delayed work.

“The improving market is driving both top line and bottom line growth in our business,” says Salah. “We believe we are in the early stages of a recovery. The pace of the recovery to date has been steady. We are optimistic that the recovery will continue into 2015.”

The company plans to continue reaching its customer base through a fully integrated program which includes print, digital, social media and face-to-face.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!

{kind=link}

{kind=link}