Building Thermal Insulation Market to be Worth More than $35 Billion by 2025

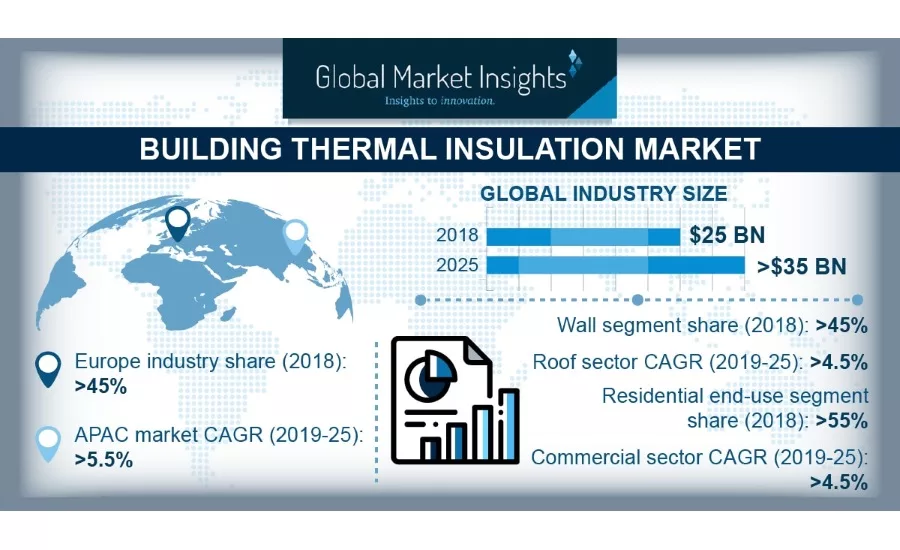

As per Global Market Insights, Inc. estimates, the global building thermal insulation market size is expected to exceed $35 billion by 2025.

Rising global energy consumption levels and the subsequent surge in demand for energy-efficient buildings are likely to fuel building thermal insulation market outlook.

The temperatures across the globe are on the rise, encouraging the implementation of sustainable, eco-friendly technologies. This paradigm shift in tandem with the rising public awareness regarding the importance of a low carbon footprint and electricity savings is expected to boost the building thermal insulation market share considerably over the estimated timeframe.

Likewise, the intensifying focus on mitigating greenhouse gas (GHG) emissions alongside population expansion will add impetus to industry forecast. Beneficial government initiatives towards housing sector development including the AHI (Affordable Housing Institute) and the Energy Company Obligation Scheme (ECO) led by the government will also assert a positive influence on market expansion.

Building thermal insulation products have sophisticated thermal characteristics which help maintain the required temperature and minimize costs of heating or air conditioning across myriad end use application sectors including residential, commercial and industrial.

The wool materials segment including stone wool & glass wool dominated the global building thermal insulation market in 2018, accounting for over 50 percent in volume share. High thermal conductivity and significant compression strength of the products are expected to present lucrative opportunities for augmenting the industry trends.

Stone wool and glass wool are non-flammable, highly adsorbent and display exceptional resistance characteristics, thereby promoting their usage as insulation materials across several applications in the commercial and industrial sectors.

On the other hand, the closed cell materials segment held over 40 percent of the market share in 2018. The segment’s application outlook is augmented by myriad factors including relatively high per unit strength and exceptional moisture and thermal resistance properties, among others.

With respect to the application spectrum, the roof segment is set to grow at an appreciable CAGR of over 4.5 percent through 2025. Subsidies, tax benefits and similar beneficial government initiatives are likely to propel building thermal insulation market demand in the segment.

For example, the Energy Efficiency and Conservation Authority of New Zealand, offers exemptions covering nearly two-third of the ceiling and underfloor areas under the Warmer Kiwi Homes program, in order to boost the utilization of thermal padding and renewable materials in constructions.

Up & coming Chinese companies are also offering roofing materials at economical prices, driving up industry demand from the roof application segment.

In terms of end-use applications, the residential segment is anticipated to account for more than 50 percent of the building thermal insulation market share through 2025, owing to strengthening customer buying power, focus on minimizing carbon footprint and energy conservation. Thermal padding products are witnessing a surge in demand as a result of persistent focus on prevention of heat flow from one side of the insulation to the other in buildings and small houses.

On the regional front, the APAC market is poised to exhibit considerable revenue growth of over 6 percent through 2025, as a result of the burgeoning construction and industrial sectors in the region. Proliferating demand for malls, convenience and grocery stores has contributed heavily towards the rising popularity of building thermal insulation products. Key players in the industry are making substantial investments towards R&D efforts for polystyrene padding development to be used in myriad applications like wall furring or cavity walls, augmenting product demand in the commercial segment

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!