For What it's Worth

As I write this article in late March, the Chairman of the Federal Reserve Board, Ben Bernanke, presides over his first meeting of the Federal Open Market Committee, the group that sets interest rates. The committee has just announced that they are continuing the gradual interest rate-raising campaign. It was the fifteenth such increase since the Fed started tightening credit in June 2004. The prudent building supply company owner has to ask himself at what point will rates hurt his business.

Last month, we executed the sale of three building supply distributors, each of which had several problems and/or poorly defined opportunities. These issues, had they gone uncorrected, would have substantially deflated the value of their companies. They were the lucky ones. I was inspired to write this article after witnessing all too many companies selling at less then fair market value.

We find that most owners operating in the building industry are salt-of-the-earth people. Our average building industry client started his or her business 20 to 30 years ago. They mortgaged their house and/or borrowed money from relatives. They worked 16-hour days, at the neglect of their family, while never really sure if they would succeed. Thirty years later, they have fed their families and put their kids through school from the proceeds of their business. Many of them still have dirty fingernails despite the fact that they can afford to run their business from the Bahamas. There is no doubt that they know the industry and its players extremely well. However, they have little or no idea how to maximize the value of their company, neither pre-sale nor at the time of divesting. At the risk of sounding insolent, most don't ever consider the critical issues that can net them as much as double the value for their life's work.

This article introduces just a few issues that may make a substantial difference in the value of your company when it comes time to sell. My objective is to ensure that the reader understands that there are several considerations that will impact the entities' value and to encourage the perspective seller to put as much effort into the selling process as they have into their company's operations. After all, the average selling process lasts about one year but when executed correctly, can yield as much as the total cumulative earnings that the owner has made over the life of the company.

Four common value deflators

- Negotiations limited to one buyer: I can't tell you how many times I have heard a business owner say, "I know what my company is worth" or "as long as I get my price, I will be happy." They think they know what their company is worth because they know what their competitor sold for or their tax accountant "did a valuation." Most merger and acquisition professionals have access to industry sales data from around the country with a sample size in the hundreds or thousands, yet every M&A professional will perform a detailed valuation prior to an offering. The high end of the valuation range can be as much as double the low end (i.e. $10 to $20 million) with a common range being about 50 percent that of the low end estimate (i.e. $10 to $15 million).

So why is the range so large? There are several reasons for this, such as:

- The potential strategic buyer pool is diverse with a large range of synergies.

- The growth opportunities of the company are difficult to forecast.

Regardless of the reason, if the M&A firms are valuing the company with a 25 to 50 percent range, then why would the owner of a building supply company think he can value the company with any better level of accuracy? The fact is, one can do all the valuations in the world but ultimately the company will be worth what the market is willing to pay. The only real way of knowing what the market will pay is to secure multiple bids and play them off against each other. We have a saying in the industry, "one bidder is no bidder, he is a dictator."

An illustration of a real world example will effectively drive this point home. Recently, our firm executed the sale of a $40 million building supply distributor. Figure 1 details the offers. As one can see, the net present value of the offers range from $7.5 to $15.5 million. In addition, deal terms are substantially different. For one, there are both offers to purchase stock, as well as the assets in the corporation. If the company happens to be a C corporation, a sale of stock can result in a substantial tax savings. Note also that bidders consist of large strategic corporations, as well as smaller private equity groups. It is probable that the value of the post-acquisition synergies differ significantly between bidders. Finally, one should realize that each of these bidders presented multiple offer iterations before arriving at the final bid that is illustrated. Securing multiple bids provides the negotiator tremendous leverage in his ability to obtain the bidders' maximum valuation.

- Inappropriate entity structure: A relatively high percentage of companies in the building industry are incorporated as C corporations. Many of these businesses were incorporated 20 to 30 years ago when limited liability corporations did not exist or were not popular (LLCs came into existence in 1977) and Subchapter S corporations had other disadvantages. For most of these companies, there is no significant reason to be a C corporation today. When it comes time to sell the business, most owners of small company C corporations will pay double the tax that they would have paid were they an LLC or Subchapter S corporation. That's because regular corporations and their shareholders are subject to a double tax (on a sale of assets both the corporation and the shareholders are taxed) on the increased value of the property/business when the property is sold or the corporation is liquidated. By contrast, LLC owners (called members) and Subchapter S corporations avoid this double taxation on a sale of assets because the business's tax liabilities are passed through to them; the LLC or S corporation itself does not pay a tax on its income.

While many tax advisors believe that a C corporation shareholder can sell stock and not incur corporate level tax on the transaction, in reality most small business purchasers will not buy corporate stock. This is especially so in the building products industry where legal liability can be relatively high. Purchasers seek to acquire the assets of the corporation for two primary reasons:

- The purchaser receives a new, stepped up basis in the assets of the corporation equal to the purchase price.

- The liabilities of the corporation will stay with the current entity and not transfer to the purchaser.

A common misconception is that one can avoid double taxation by merely converting to a Subchapter S. When an existing C corporation converts to an S corporation, only the post-conversion appreciation in the corporation's assets will qualify for single level tax treatment, unless the corporation's assets are sold more than 10 years after the date of conversion.If your company is a C corporation and you have at least 10 years before the sale of the business, then seriously consider a conversion that will lower the taxable impact on your life's work. If you do not have a 10-year time horizon prior to the sale of your company, then hire a strong M&A advisor who will be able to assist in structuring a tax efficient transaction. The good news is that there are several methods to circumvent and/or minimize the negative tax implications resulting from the sale of C corporation assets. I will reserve a detailed discussion of these methods for a future article.

- Transferability issues: One question that every buyer will ask himself when considering the acquisition of a company is, "What are the issues that we need to overcome when transitioning the business to the new owners?" Transferability challenges are usually a result of two issues: 1) Substantial intellectual property is in the head of the owner, and; 2) the owner has a large number of close relationships that are at risk when he leaves the company.

The first issue is most common with technology-oriented companies or companies that have proprietary manufacturing processes. The second is an issue that seems to plague the building industry more often then any other industry. Many building industry owners have been around the industry for a long time or even grew up in the industry. They pride themselves on delivering top quality service and maintaining close relationships with key customers and vendors. Even when the company has grown to a substantial size, often times the owner still acts as the "customer liaison." If this sounds familiar, ask yourself the following question, "What customers will leave when I leave?" If the answer feels uncomfortable, then consider to obsolete yourself from the business. Even though your payroll will probably go up, the increased value you will get from this move should be several times more then the incremental payroll bill.

- Poor or no professional representation: As the industry consolidates, several large corporations are emerging in just about every sector of the building industry. For example, in the distribution sector, the powerhouses are Stock, Strober and Allied. In the residential construction sector, the dominant players are Pulte, Lennar, KB Homes and Toll Brothers. These dominant players are often aggressive acquirers and can often justify higher valuations. In addition, there are hundreds of private equity groups rolling up smaller players. The PEGs are professional buyers of companies. If you want to get the best price for your business, you need to get exposure to either or both the large players and PEGs. Note that in the transaction illustrated above, both buyer types were present.

Most people are familiar with the Latin phrase caveat emptor, "let the buyer beware," but few can tell you how to say, "let the seller beware." The law focuses on the buyer because it is assumed that the typical buyer needs protection. When it comes time to sell your company, it is imperative that you have some strong representation protecting your interests. That does not mean your local business broker or your CPA or corporate attorney friend. Rest assured that whether it be a large industry player or a professional PEG sitting on the other side of the table, both will have extremely strong legal, financial and accounting representation. Even if the other side of the table is not occupied by an industry powerhouse or PEG, I advise you to inquire as to the extent of transactional experience that your attorney and CPA have. The key word here is "transactional." Most accountants are tax preparers who do not specialize in deal structuring. Likewise with attorneys, transactional expertise is a specialty within the corporate law field. Don't take it for granted. It can cost you millions.

When is the best time to sell?

There are three issues to consider when answering this question: personal preferences, business performance and the external environment. It is rare that all three of these issues are aligned. Most owners allow personal preferences to dictate timing. Savvy owners will sell when business performance is on the rise, although we see too many owners selling their business when times are tough. It is the rare individual that has the foresight or luck, whatever the case may be, to time all three variables. Rather then get into a detailed discussion on timing, I suggest that the reader visit www.lockebridge.com/article2.htm for a brief article on the topic. I will however write briefly about the economic variables relevant to the building industry.Building industry economics

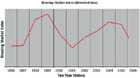

Mergers and acquisitions activity in the building industry is running high these days, as owners have now enjoyed numerous substantial growth years. However, as most business owners in the building industry are aware, the prime rate and the federal funds rate are at their highest since the spring of 2001. The National Association of Home Builders Market Index, a measure of builder sentiment, fell to 55 in March, the lowest figure since April 2003. At the same time, mortgage applications, as measured by the Mortgage Bankers Association, have fallen five out of the past seven weeks. According to Wachovia in its March 2006 article "Housing Starts Surprises Again":"The housing market is slowing and should continue to do so throughout 2006. We are currently forecasting 1.93 million housing starts in 2006. This figure indicates a market slowdown but a relatively soft landing."

What does this mean to the value of your company? It is obvious that increasing rates tend to have a negative impact on housing starts. When housing starts slow, it can have a severe impact on the profitability of the building supply industry. However, the impact of rates on business profitability is only half the story. All things being equal, the business valuations also decline when rates go up. This happens because alternative fixed income investments yield higher returns as rates increase. A few weeks ago, I was speaking to a group of building supply business owners when one owner said, "Increasing rates are bad for the stock market but don't impact us little guys." The fact is that increasing rates put pressure on equity values regardless of the size of the business. So, increasing interest rates in the housing market can do some real damage on valuations because it can substantially hamper business performance while at the same time put downward pressure on valuation multiples.

Conclusion

There are two things all business owners must do: file tax returns and exit their business. If your exit is a sale, as opposed to bankruptcy or gifting, then you owe it to yourself to become educated on those issues that can impact the company's value. You may even decide to hire someone to "polish the business" prior to selling.The execution of a transaction at a favorable price can require a substantial amount of experience, as well as consume a great deal of resources. A deal team (attorney, accountant and merger and acquisition advisor) with significant transactional experience can be one of the best investments you will ever make.

Finally, as the saying goes, "timing is everything." Only you can decide when to sell your company. An understanding of business opportunities, as well as industry and economic dynamics, is essential in determining when valuations will be highest. The National Association of Home Builders' housing market index (a weighted, seasonally adjusted statistic derived from ratings for present single-family sales, single-family sales in the next six months and buyer traffic) has seen five consecutive years of growth through the end of 2005. A significant decline in the index over the last five months indicates a continued slowing in the housing market. With this said, who really knows what the future will bring. There does seem to be a relatively high level of uncertainty in the industry, so if your time horizon is relatively short, less than five years, you may want to consider selling in the near future while merger and acquisition activity is strong and there is an abundance of money searching for good companies.

If you read this article, please circle number 332.

Sidebar: A few other popular deflators

- Environmental issues

- Poor financial or accounting records

- Outstanding legal issues

- Bogus representations or forecast

- No management depth

- No or unclear growth opportunities

Links

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!