Construction Economic Forecast

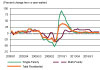

The current residential downturn has been the deepest and longest on record in the nation’s history. With 12 quarters of real residential construction put-in-place year-over-year declines, including 10 double-digit year-over-year drops, everyone is wondering when the market will turn up. Every new quarter brings promise of an upturn yet ends with further weakening. Just how low can the market go?

So far the market has proven itself extremely flexible. In the first quarter of 2009, real residential construction spending reached $1.98 billion, 59 percent lower than the market’s peak in the second quarter of 2006. This recession is particularly remarkable when compared to the last major peak-to-trough drop during 1994-95 in which real residential expenditure fell 13.1 percent.

According to IHS Global Insight’s June 2009 U.S. National Monthly Construction Briefing forecast, the second quarter will not see an upswing (as of press time) and plunge to a new low of $1.67 billion in spending, down 65.3 percent from the peak. Following the second quarter of 2009, however, the market is expected to experience positive quarter-to-quarter growth. Nonetheless, even by the end of 2018, total residential construction spending will reside at $4.02 billion, below its previous peak of $4.8 billion.

Most key indicators of housing activity (home sales, housing starts and permits) are showing signs of stabilization, based upon dramatically improved affordability-for those who can qualify for credit. Housing starts, one of the main drivers of real residential spending, are expected to hit bottom in the second quarter. Recovery in residential construction spending tends to lag that of housing starts. Despite the delay, real residential construction spending should start to rise on a quarter-to-quarter basis by year-end.

On the policy front, only 55,000 loan modifications were offered during the first two months of President Obama’s ambitious $75 billion Homeowner Affordability and Stability Plan, and few lenders were agreeable towards lowering outstanding balances. The program needs to take off soon; otherwise falling house prices and rising unemployment rates will reduce the eligible pool. Further, Fannie Mae and Freddy Mac’s serious delinquency rates for conventional single-family homes are climbing at troubling rates. Fannie’s rate jumped 19 basis points to 2.96 percent in February, up from 1.1 percent during the same time last year. The delay in the Homeowner Affordability and Stability Plan, and troubles in Fannie Mae and Freddy Mac, threaten the outlook for residential construction by stifling demand and building up supply.

REAL RESIDENTIAL CONSTRUCTION SPEND MARKET

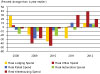

Total residential construction spending can be divided into three main categories: single-family, multi-family, and improvements. In the first quarter of 2009, single-family construction represented 43.1 percent of total residential construction. This share has been slowly declining since the third quarter of 2005 when single-family construction accounted for 71.8 percent of total residential construction spending. Improvements follow single-family construction in terms of share with 42.4 percent, and multi-family trails with 14.5 percent. Single-family construction has been the main contributor to the downturn in residential construction, swiping 22 percentage points off total residential construction growth in 2008.Multi-family construction spending has not taken the same deep dive as single-family, at least not yet. Looking at the 61.7 percent jump in multi-family starts in May, one might assume the multi-family market to be in recovery. However, this increase was not as significant as multi-family housing starts tend to be volatile.

Multi-family permits, which better gauge underlying conditions, posted its 11th consecutive monthly decline, falling 8.3 percent to a record low of 110,000 units (annual rate). The recent sharp decline in this market is likely related to financing. Some builders are overwhelmed with debt, while others cannot find funding to finance projects with positive net present values. For these reasons, the multi-family construction outlook is grim. The first quarter of 2009 shows multi-family expenditure dropping 7.5 percent from a year ago, and annual declines will be in double digits from the second quarter of 2009 through the first quarter of 2011.

RESIDENTIAL CONSTRUCTION LINKED TO COMMERCIAL CONSTRUCTION

Residential construction is closely linked to commercial construction. In general, when there is an upturn or downturn in residential construction, commercial construction tends to follow with similar growth patterns at least three quarters later.IHS Global Insight defines commercial construction as a composite of office, lodging, retail, automotive, and warehousing. During this construction recession, the residential sector contracted in terms of real year-over-year growth in the second quarter of 2006, while the commercial sector saw its first year-over-year decline in the fourth quarter of 2008.

The commercial construction boom has ended as the need for extra retail and office space has evaporated. Commercial construction spending was stable as ongoing projects were completed, but lack of available financing for commercial real estate, coupled with sharp pullbacks in consumer spending and rising unemployment, made further investment in commercial construction untenable. In addition, delinquency rates on commercial real estate loans are climbing and will rise much further. This increase poses a threat to recovery, since it will affect bank balance sheets and lending to finance new buildings. Consequently, a downward trend in construction spending remains for commercial construction such as retail developments, offices and hotels.

PROSPECTS FOR INDIVIDUAL SECTORS ARE BLEAK

After retreating 1.2 percent in March and 0.2 percent in April, retail sales advanced 0.5 percent in May. A price-driven 3.6 percent jump in sales of gasoline accounted for over half of the May increase in total sales, and discretionary spending remained weak. The slight improvement is a positive sign, but it will not do much to dispel the downward momentum in retail construction spending, which will rebound only after significantly stronger gains in retail sales.Shopping malls are losing tenants as retailers continue to close stores, and even if it were possible to secure financing, empty retail complexes create little incentive for new builds. Real retail construction spending in the U.S. is expected to tumble 32.6 percent in 2009 and 13.9 percent in 2010. The sector’s performance will be fairly consistent across all states with declines ranging from 29.4 percent in New Hampshire to 35.9 percent in Arizona.

The ongoing national economic downturn, which has severely cut into payroll employment and household wealth, has made consumers cautious about recreational spending on activities such as travel. Businesses too have reduced travel in an effort to control spending. The result is declining demand for lodging and excess supply. Overcapacity and a frozen securitization market for commercial loans have put many projects in jeopardy and will hinder lodging construction in the near-term. Construction spending is expected to slide 39.5 percent in 2009 and 46.3 percent in 2010.

The overbuilding following the 2002-03 recession and recent massive monthly layoffs will prevent growth in office construction in the next couple of years. The national unemployment rate, which currently sits at 9.4 percent, is expected to climb until mid-2010 when it will reach a peak of 10.4 percent. Monthly payrolls in May fell by 345,000, which was much less than expected and far better than the 741,000 jobs cut back in January. The moderation is a positive sign, but a monthly loss of more than 300,000 jobs is by no means negligible, and office construction spending will feel the effects.

In summary, the residential upturn is in sight, and the recovery will be strong with 11 quarters of double-digit year-over-year growth expected beginning the second quarter of 2010. The commercial sector will continue to decline for four more quarters, while the residential market recovers in the second quarter of 2010. Though the residential recession is to be longer than the commercial recession, the commercial trough will be just as deep. W&C

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!

.webp?height=200&t=1747405774&width=200 "ACA(1).png")